The 2006 SEC and 2010 Dodd-Frank mandated executive pay proxy disclosure requirements significantly increased the amount of information that companies must disclose, and shareholders and other interested parties must navigate to determine a company’s executive compensation program. The SEC’s June 26, 2025, Roundtable gave voice to many of the positive and negative attributes to the current proxy disclosure regime, with near universal support for ensuring the disclosed information is more readily accessible and material to investors’ understanding of the program. While many commentators expressed concerns about the complexity of the Pay versus Performance (PVP) disclosure rules and some cited the lack of interest in this disclosure, others welcomed the disclosure, as it provides investors with an analysis of outcome-based compensation compared to performance rather than the static view of compensation reported in the Summary Compensation Table (SCT). Indeed, the main reason Dodd-Frank mandated the PVP disclosure was the failure of the 2006 rules to provide investors with a true, consistent picture of pay and performance.

In making comparisons of pay to performance outcomes, PVP is more fit for purpose — via Compensation Actually Paid (CAP) — than the SCT total compensation. As the exhibit below shows, there are many adjustments to SCT total compensation to arrive at CAP. These include the replacement of the grant date fair value of equity awards granted during the year with “mark to market” and forecasted performance changes in the value of previously granted equity awards.

This required disclosure has helped external parties rely less on SCT total compensation in pay-for-performance comparisons, a purpose for which it is ill suited due to its static nature. For most companies, there are now 5 years of PVP data to show a company’s compensation and performance over time. This helps alleviate some of the pay and performance disclosure “pressure” in more difficult performance years because there is already a standardized starting point for showing the impact of stock price and financial results on NEO pay over several years. The PVP disclosure rule has its challenges, but a number of suggestions provided in comment letters that have been submitted to the SEC, if adopted, would streamline the disclosure, reduce the reporting burden on companies and make it more user-friendly.

The Wall Street Journal published an article on August 5, 2025, on the PVP/CAP methodology that demonstrated to shareholders its superior pay-for-performance explanatory power relative to SCT total compensation.

Pay Governance's research, including the four Viewpoints cited below, have found CAP to be flawed but better to use than SCT total compensation for developing conclusions regarding pay-for-performance alignment.

Key Findings / Observations:

Shareholders and companies may find the results of our comparison of CAP, as presented in the new PVP tables in 2023 proxy statements and realizable pay (RP) of interest for the following reasons:

We believe RP can provide Compensation Committees with additional insights when evaluating pay for performance than tools based on the SCT or even PVP methodologies and should be a consideration in addressing this important corporate governance issue.

Publication: May 2023

Viewpoint: Utilizing Compensation Actually Paid to Evaluate Pay and Performance

Key Findings / Observations:

Based on our analysis, there are several key takeaways that shareholders and companies may find of interest:

Publication: June 2023

Viewpoint: Does Compensation Actually Paid Align with Total Shareholder Return?

Key Findings / Observations:

• There is a strong correlation (.56) between relative TSR and CAP but not between TSR and SCT Compensation (.08)

• A relative rank analysis against a company’s peer group or industry- and size-specific index provides the most useful evaluation of the relationship between CAP and company TSR

• A disconnect between relative CAP and TSR may be traceable to competitive deficits/ surpluses in executive compensation strategy and policies, which may need to be addressed

Publication: August 2024

Viewpoint: Demonstating Alignment of CEO Pay and Performance

Key Findings / Observations:

Publication: February 2025

From our July 2024 Viewpoint, Figure 1 below is based on 159 S&P 500 companies and plots each one based on their difference in percentile ranking of 4-year cumulative TSR and 4-year cumulative SCT compensation. The three-shaded areas represent companies where relative TSR performance and SCT compensation percentile ranking are within 25 percentile points (green zone), TSR percentile ranking exceeds SCT compensation ranking by > 25 percentile points (yellow zone), and TSR percentile ranking is below SCT compensation ranking by > 25 percentile points (red zone).

When the same analysis is performed using CAP rather than SCT total compensation, the alignment of pay and performance improves dramatically as shown in Figure 2 below.

The PVP/CAP disclosure provides a consistent approach for comparing NEO pay and performance over time, on an absolute basis and relative to peers. Companies should continue to evaluate and apply the most relevant perspectives, such as multi-year incentive payout history, realizable pay and actual/realized pay compared to TSR/primary financial metrics, in the design and analysis of the pay and performance structure and resulting outcomes. Companies also need to ensure the CD&A clearly summarizes these pay-for-performance perspectives in the context of the industry as well as company-specific challenges and opportunities that explain the pay decisions made for the most recently completed performance periods to provide investors a complete picture.

_______________

Read More

.svg)

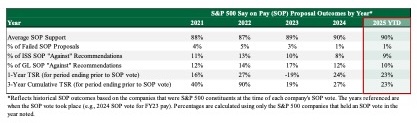

Pay Governance has gathered information on Say on Pay (SOP) proposal outcomes and total shareholder return (TSR) for S&P 500 companies dating back to when SOP began with the 2011 proxy season. This article places into context how the most recent 2025 SOP outcomes are unfolding compared to recent history beginning in 2021. In both 2024 and 2025, we found that, overall, companies had greater SOP success, with proxy advisor opposition to SOP proposals and the number of companies failing SOP at record lows. Although the year has not yet ended, about 90% of S&P 500 SOP proposals have already been put to a shareholder vote through August 31, 2025.

Average shareholder support for S&P 500 SOP proposals has been strong and relatively stable over the past 5 years at 87%-90%. Our analysis of 2025 SOP outcomes shows a failure rate and proxy advisor “against” rate that are generally in line with 2024 levels (and below pre-2024 levels). The 2025 SOP failure rate is tracking at 1%, which is comparable to 2024 (also 1%) but below the 3%-5% rate observed in 2021-2023. Similarly, 2025 proxy advisor opposition to SOP proposals is below pre-2024 levels. Notably, Glass Lewis’ 2025 “against” recommendation rate is at an all-time low of 10%.

The lower rate of failed SOP proposals and proxy advisor opposition may be attributed to a continuation of strong TSR performance through fiscal year-end 2024. Further, many companies are increasingly receptive to shareholder feedback on executive pay programs and are taking meaningful actions in response. In addition, large institutional investors are increasingly less dependent on proxy advisors.

Exhibit 1: S&P 500 SOP Proposals by Year (2021-2025 YTD)1

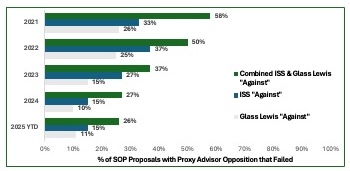

Not only are fewer SOP proposals being opposed by proxy advisors, but the impact of proxy advisor opposition has also dwindled in recent years. As shown in Exhibit 2, we demonstrate proxy advisor impact by the percentage of proposals that fail when an “against” recommendation is issued. In 2021-2022, when ISS opposed SOP, about 35% of the proposals received a failing vote. During this same period, when Glass Lewis opposed SOP, about 25% of the proposals failed. We began to observe a step-down in 2023, with the percentage of failed proposals decreasing to 27% for those opposed by ISS and 15% for those opposed by Glass Lewis. For 2024 and 2025, the percentage of companies failing SOP further dwindled to 15% for ISS and about 10% for Glass Lewis. When both proxy advisors recommend “against” SOP, we observed a more dramatic decline. In 2021, over half (58%) of SOP proposals failed when they were opposed by both proxy advisors; this decreased to about one-quarter (26%) in 2025.

Exhibit 2: Proxy Advisor SOP Opposition Impact (2021-2025 YTD)1

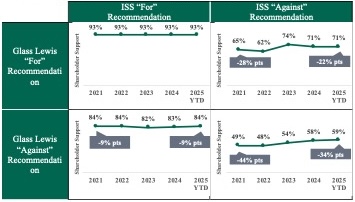

Despite the decline in proxy advisor-opposed SOP proposals that ultimately failed, proxy advisors continue to have a meaningful influence on shareholder support levels. As shown in Exhibit 3, when both proxy advisors recommend in favor of SOP proposals, average shareholder support has remained steady over the past 5 years at 93%. However, when both ISS and Glass Lewis oppose SOP, average shareholder support levels were reduced by -34 percentage points in 2025 (compared to a -44 percentage point reduction in 2021). The influence of ISS opposition on SOP support levels has diminished from a negative impact of -28 percentage points in 2021 to -22 percentage points in 2025. Glass Lewis influence on SOP outcomes has been relatively constant at a -9 percentage-point difference in both 2021 and 2025.

Exhibit 3: Proxy Advisor Influence on SOP Support Levels (2021-2025 YTD)1

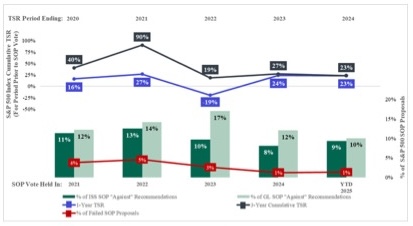

As shown in Exhibit 4, we observed an improvement in the correlation between TSR performance and SOP outcomes for proposals held during 2024 and 2025. S&P 500 TSR performance was relatively strong for the periods ending prior to the 2024 and 2025 SOP proposals and reflects an improvement over TSR performance observed prior to 2023 SOP proposals. In 2024 and 2025, we observed commensurate declines in failed SOP proposals and proxy advisor SOP opposition compared to 2023. Findings from our previous Viewpoint titled, “The 2023 Say on Pay Season – Outcomes and Observations,”3 showed that the 2022 and 2023 SOP outcomes ran counter to the premise that TSR performance should be correlated with SOP proposal success.

Exhibit 4: 1- and 3-Year Cumulative TSR2 and SOP Outcomes1 (2021-2025 YTD)

Overall, S&P 500 SOP outcomes have shown both improvement and greater stability in recent years, with 2025 failure rates and proxy advisor opposition similar to 2024 levels and below pre-2024 levels. The data suggest a stronger correlation between TSR performance and SOP outcomes in more recent years, particularly in 2024 and 2025, where sustained TSR performance is aligned with improved SOP results.

We have seen the influence of proxy advisors diminish in recent years, as measured by the conversion rate of proxy advisor “against” recommendations that ultimately result in failed SOP proposals. However, proxy advisors continue to have a meaningful influence on the level of shareholder support, particularly when both proxy advisors unite in opposition.

For 2026, Glass Lewis is making significant changes to its pay-for-performance methodology, a key input to its determination of SOP recommendations. It remains unknown how this may impact the Glass Lewis rate of SOP opposition and overall influence on shareholder vote levels of SOP proposals, but we will continue to monitor this development in the coming year.

Read More

Recent statements and opinions made by proxy advisors, a Europe-based institutional investor, and some academics and consultants have cast the preference for using performance-based equity incentives into question. The use of these plans, such as performance share units (PSUs), has become nearly universal and is the largest form of compensation delivered to S&P 500 chief executive officers (CEOs). This practice has largely been due to previous proxy advisor requirements, and investor preferences, that PSUs or other performance-vesting equity comprise at least a majority of CEO total equity compensation.

As demonstrated in this Viewpoint, our investor opinion survey conducted this summer shows that the vast majority of shareholders strongly prefer that companies continue the majority usage of PSUs, and it does not indicate much preference for movement to long time-vesting restricted stock units (RSUs). Our survey conducted in partnership with IR Impact of more than 100 large investors revealed:

The recent criticisms of the use of PSUs have largely focused on three themes:

In response to some of these criticisms, both Institutional Shareholder Services (ISS) and Glass Lewis have included topics in their annual policy surveys asking survey participants for their opinions on the use of performance-based and time-based equity plans, including the relative emphasis preferred on both vehicles. To date, the proxy advisors appear to be mixed/ambiguous on this important topic.

The ISS 2024 policy survey indicated that a minority (31%) of investors thought ISS should revise its current approach and begin considering the use of time-based equity awards with extended vesting periods to be a positive mitigating factor when there is a pay-for-performance misalignment. A larger group of investors (43%) responded that a predominance of time-based equity awards should continue to be viewed as a negative factor in the context of the presence of pay-for-performance misalignment.[3] In contrast to these results, ISS has also stated “many investors are calling into question the presumption that performance-conditioned pay is preferable to other forms of executive pay.”[4]

The Glass Lewis 2024 policy survey more directly asked investors about their preference of LTI vehicles. Only 15% of investors agreed that they “prefer time-based equity awards over performance-based equity because the vesting conditions for performance-based equity have become too complicated and difficult to monitor.” As further evidence of investor support for PSUs, the Glass Lewis survey results indicated that 92% of investors agreed “a large portion of equity compensation should be performance-based to ensure that executive pay is aligned with performance results.”[5]

Likely influenced by the proxy advisor pay-for-performance models, 93% of S&P 500 companies use PSUs; these plans on average make up about one-third of CEO target total compensation.[6] There clearly was and has been strong shareholder support for the CEO pay model as evidenced by high average Say on Pay votes (2011-2024 average S&P 500 “for” vote of 90% and 98+% of votes passing).[7]

Recent regulations to require the Compensation Actually Paid (CAP) disclosure in the proxy also helped support the notion that CEO pay has been aligned with performance. Pay Governance research on PSU plan payouts and TSR performance confirmed that PSU payouts are aligned with shareholder outcomes. This may partially explain why shareholders have consistently and strongly supported Say on Pay since its inception. As further support against the above criticisms of PSUs, Pay Governance and a few others extensively studied the PVP/CAP 2022 regulation and found it to demonstrate very strong pay and performance alignment. If CAP is high or growing, it will be aligned with TSR and the obverse will also be true (low/decreasing CAP aligned with low TSR).[8]-[10]

Pay Governance in collaboration with IR Impact, a leading governance and investor relations intelligence firm, surveyed more than 100 institutional investors and public pension funds with aggregate assets under management (AUM) of $29 trillion. Our objective was to understand investor perspectives on the use, design, and disclosure of PSUs given recent media coverage of this important and prevalent compensation component. While the design and mix of LTI awards need to be driven by each company’s unique cultural and strategic situation, understanding investor preferences is also critical.

Our survey sample included institutions with an average AUM of $261 billion and included responses from portfolio managers, investment analysts, and governance/stewardship officers. The participants were based across North America (59%), Europe (40%), and Asia (1%).

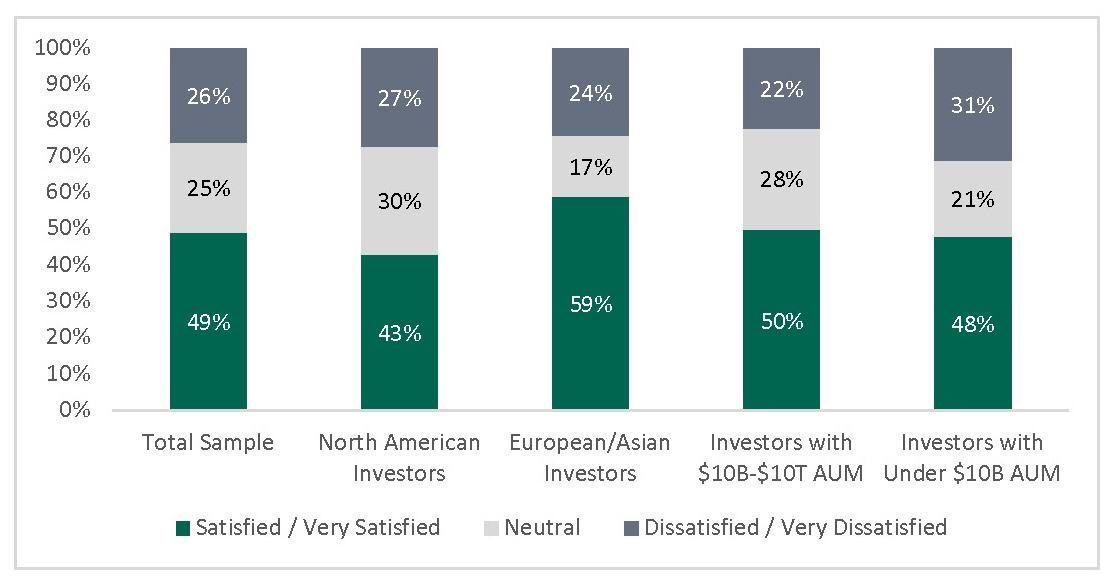

In general, our survey respondents expressed satisfaction that executive pay is aligned with shareholder performance, much of which is explained by the large amounts of PSUs granted (see Exhibit 1). Nearly one-half (49%) of all investors indicated they were satisfied / very satisfied with the CEO pay alignment at their portfolio companies while only about one-quarter (26%) were dissatisfied or very dissatisfied. Investor sentiment was similar across regions and AUM.

Exhibit 1: Investor Sentiment Toward Executive Pay and Performance Alignment

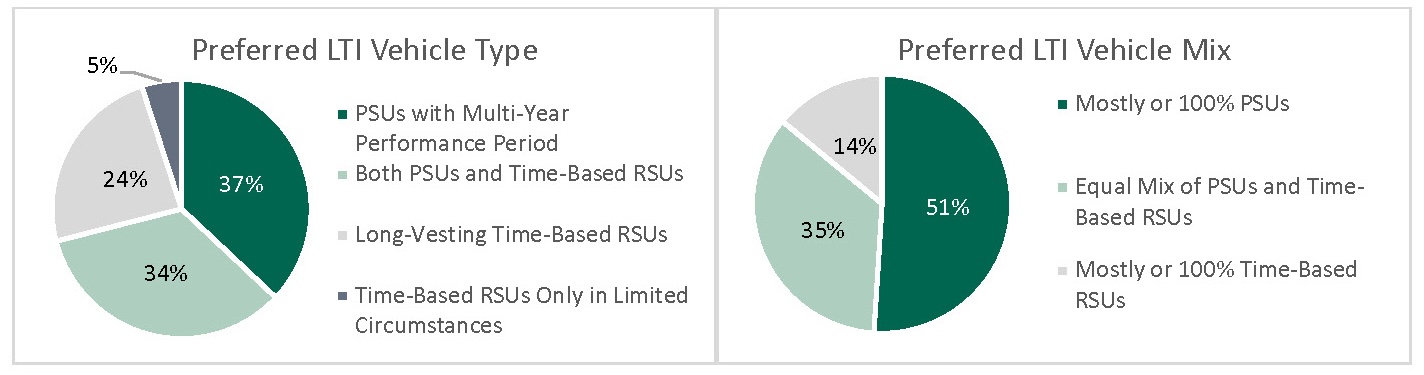

As shown in Exhibit 2, the results of our survey largely support the preference for PSUs in contrast to time-based stock awards (RSUs) with longer vesting schedules than typical: 71% preferred PSUs that would be earned/vested over a multi-year period or PSUs in concert with a balance of time-based RSUs. A majority (51%) would rather have issuers award mostly or 100% PSUs, while a sizeable group (86%) desire that PSUs comprise at least 50% of total LTI value. Importantly, from most executives’ point of view, the upside payout of the number of PSUs (150-200% of target) is extremely compelling and motivational relative to RSUs that do not have that type of upside. Investor opinions are split on whether standard stock options with time-vesting are considered performance-based (52%) or time-based (48%).

Exhibit 2: Investor Preferences of LTI Vehicles

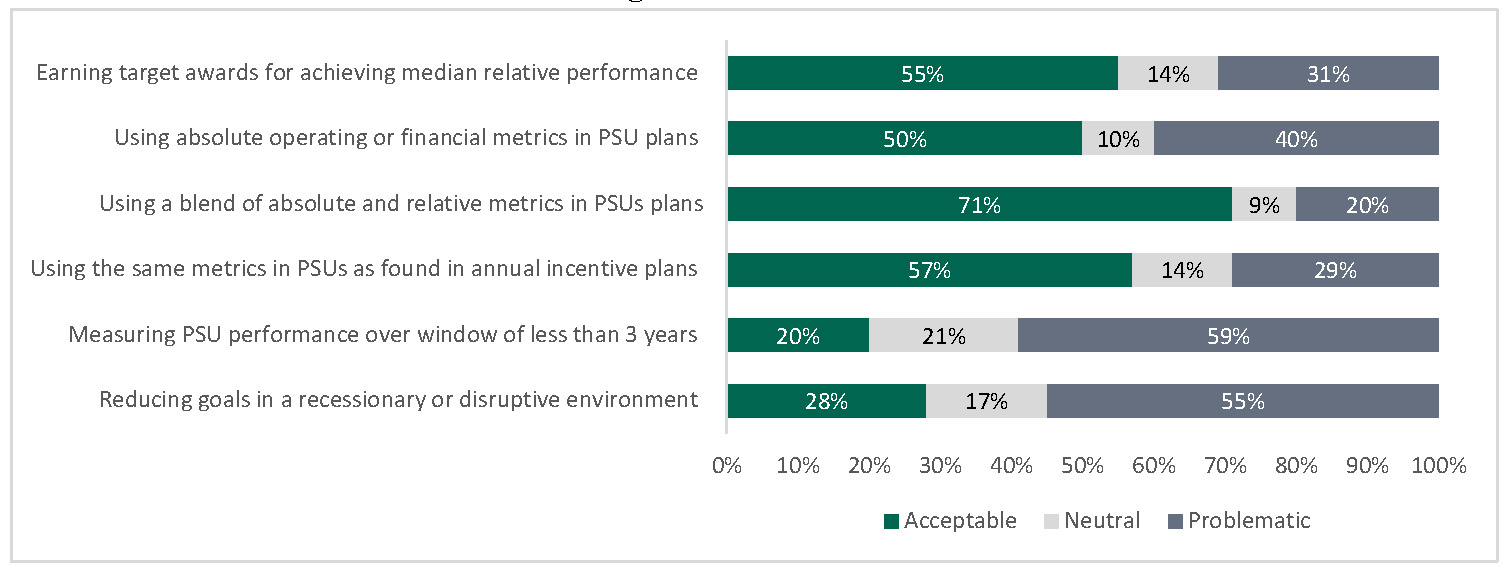

From a design and disclosure perspective, investor preferences from our survey generally mirror current typical practices (see Exhibit 3). Such practices include paying out at target for median (50th percentile) relative performance, using a blend of absolute and relative metrics (some of which may overlap with annual incentive metrics), and measuring PSU performance over a multi-year period of at least 3 years. In terms of PSU metrics, most (91%) investors prefer financial metric(s) linked to the issuer’s disclosed strategy or a mix of financial metrics and stock-price metrics (absolute or relative). The majority (55%) of respondents indicated it would be problematic to lower performance goals year-over-year in recessionary or disruptive environments. Lastly, and in contrast to common practices, most investors (84%) agree that issuers should forward-disclose PSU multi-year financial performance goals in their CD&As. Based on information collected from ESGAUGE, we found that of the S&P 500 companies that use 3-year financial metrics, 40% forward-disclosed their goals in 2025 proxy statements.

Exhibit 3: Investor Preferences of LTI Design and Disclosure Practices

Pay Governance reviewed the shareholder engagement efforts disclosed by nearly 200 S&P 500 companies in 2024 and 2025 proxy filings and extracted investor feedback related to LTI programs.[11] The most frequently cited areas of investor feedback on LTI programs were around design features of PSU plans (e.g., types of metrics used, length of the performance period, difficulty of the performance goals). The next most common area of investor feedback was around the mix of LTI vehicles and, more specifically, the proportion of LTI denominated in PSUs. When commenting on the use of PSUs, most investors expressed strong support for PSUs to increase the alignment of executive compensation with Company performance and, in some cases, conveyed the preference for the majority of LTI value to be delivered in PSUs.

Anecdotal criticisms of PSUs should be considered thoughtfully and not compel a change in approach. Rather, it is important to have a clear understanding of the preferences of shareholders and to ensure the LTI program supports long-term strategic priorities and aligns with the company’s executive pay and performance philosophy. Most companies can and likely will continue with the vast majority of their executive pay practices, as they have been highly motivational, aligned with stock price performance, very successful, and endorsed by the shareholders.

__________________________

Read More

We simplify the complexities of the executive pay process. Our consultants are skilled at helping clients design and administer programs that appeal to reason, hold up under scrutiny, and successfully link executive pay to shareholder value.

View all services

Our book discusses many aspects of executive compensation — contemporary and emerging program design, administration, and governance of programs — based on our extensive research and experience.

Download The e-book

Our first book is aimed to help our clients create alignment between a highly motivated executive team and long-term shareholder value creation.

Download The E-BOOK